The term “rare earth elements” (REEs) evokes images of cutting-edge technologies—electric vehicles, wind turbines, smartphones, and advanced defense systems. Yet, the story of these critical minerals began over two centuries ago, in the late 1700s, when Swedish chemist Carl Axel Arrhenius discovered a dark mineral in a quarry near Ytterby. This mineral, which he named “ytterbite,” would later be found to contain several previously unknown elements. Over the 19th century, chemists isolated many more rare earth elements, gradually expanding the group we now recognize as essential to the modern economy.

For much of the 20th century, REEs were confined to niche applications like color television, glass polishing, and catalysts. But with the acceleration of digital and green technologies, their demand has surged. Today, rare earths are indispensable in everything from electric motors and energy-efficient lighting to lasers, medical devices, and aerospace systems.

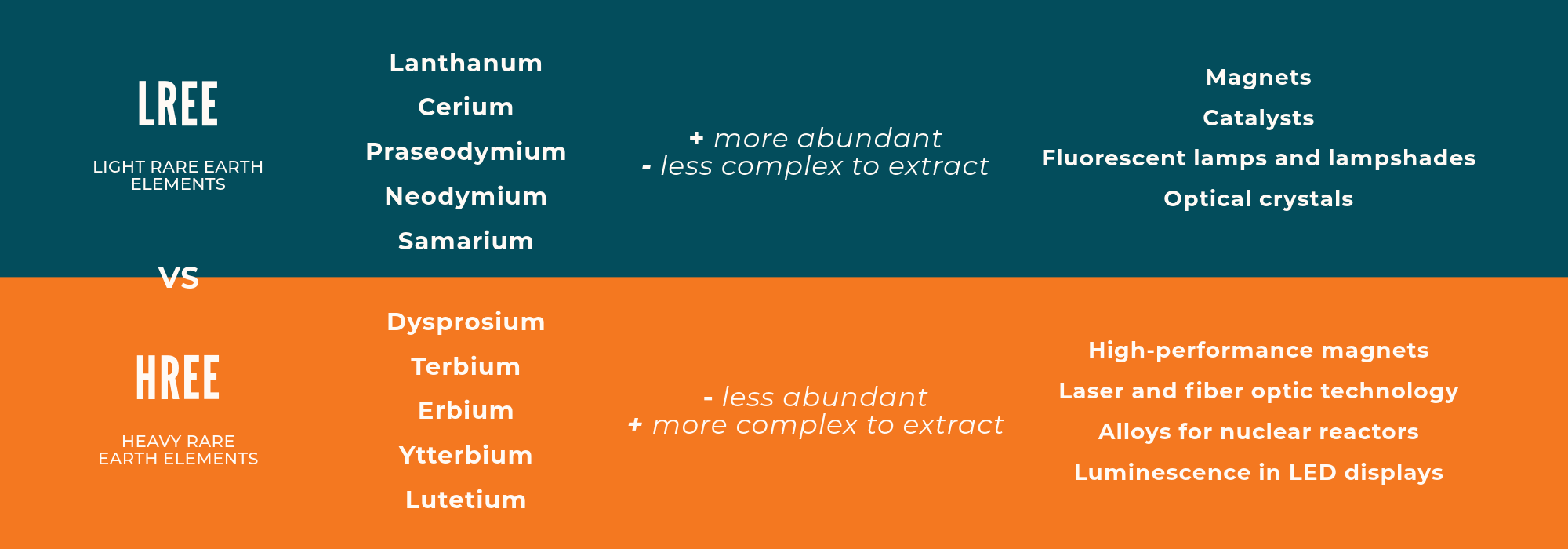

Despite being grouped together, rare earth elements are not all the same. They are commonly classified into two subgroups: light rare earth elements (LREEs) and heavy rare earth elements (HREEs). This technical distinction carries meaningful implications for mining economics, market dynamics, and strategic value.

LREEs include elements like lanthanum, cerium, praseodymium, and neodymium. These elements are more abundant in the Earth’s crust and are typically found in higher concentrations within most known deposits. They play a vital role in modern technologies, such as permanent magnets (used in electric motors), automotive catalytic converters, and high-performance glass. Because of their relative abundance and established supply chains, LREEs are more commonly mined and tend to have more moderate prices.

HREEs, on the other hand, are far less common and more difficult to extract economically. This group includes elements like dysprosium, terbium, ytterbium, and lutetium, as well as yttrium and scandium, which share similar properties. These metals are critical for high-performance applications where efficiency, thermal stability, and miniaturization are essential. They are used in high-temperature magnets for electric vehicle drivetrains, wind turbine generators, LED displays, precision sensors, and military-grade systems.

What makes HREEs particularly strategic is not only their scarcity but also their irreplaceability. Substitutes, when they exist at all, often result in lower performance or higher costs. As such, these elements are seen as essential to national security and economic independence, particularly in jurisdictions looking to diversify away from concentrated global supply chains.

From a mining perspective, deposits that contain a meaningful proportion of HREEs offer a differentiated opportunity. Even in cases where the primary operation targets another mineral—such as ilmenite for titanium dioxide—HREEs can be recovered as a valuable byproduct. This integrated recovery model often allows for lower extraction costs and increased revenue resilience, as the project benefits from exposure to multiple commodity markets.

For investors, understanding the balance of light versus heavy rare earths in a given resource is essential. A deposit rich in heavy rare earths is not just a mineral asset; it is a gateway to critical technologies, stable demand, and potentially higher long-term margins. In an era where clean energy, electrification, and digital infrastructure are redefining industrial priorities, these elements are more than just rare—they are strategically indispensable.